Test Equipment Financing & Leasing: The Complete 2026 Guide for Businesses

Test equipment is mission-critical. Whether you're running a medical diagnostics lab, an electronics manufacturing line, an aerospace quality control department, or an environmental testing facility, the precision instruments you rely on directly affect your product quality, regulatory compliance, and profitability. The problem? High-performance test equipment is expensive — often $10,000 to $500,000 or more per unit.

Test equipment financing and leasing makes it possible to access the tools your business needs without draining capital reserves. Instead of paying a large lump sum upfront, you spread costs over time — preserving working capital for operations, payroll, and growth initiatives.

This guide covers everything you need to know about financing and leasing test equipment in 2026: how each option works, what rates and terms to expect, which industries benefit most, qualification requirements, tax advantages, and how to choose the right path for your business.

In This Article

- What Is Test Equipment Financing?

- Financing vs. Leasing: Key Differences

- Types of Test Equipment You Can Finance or Lease

- Rates, Terms, and What to Expect

- How to Qualify for Test Equipment Financing

- Tax Advantages: Section 179 and Bonus Depreciation

- Industries That Rely on Test Equipment Financing

- How to Apply

- Why Choose Crestmont Capital

- Frequently Asked Questions

What Is Test Equipment Financing?

Test equipment financing is a type of equipment loan or lease that allows businesses to acquire measurement, diagnostic, calibration, and analysis instruments over time rather than with a single upfront payment. Like auto financing, you work with a lender who pays for the equipment, and you repay the lender in fixed monthly installments over an agreed term — typically 24 to 72 months.

At the end of a financing arrangement (also called an equipment loan), you own the equipment outright. With an equipment lease, you may have options to return the equipment, renew the lease, or purchase it at fair market value or a predetermined price (such as $1).

Test equipment financing is governed by the same principles as general equipment financing, but with specific considerations for:

- Residual value: Test equipment can depreciate quickly due to technological advances, affecting lease structures.

- Calibration requirements: Lenders often finance calibration services alongside the equipment.

- Soft costs: Installation, training, and software licenses can often be bundled into the financing.

- Technology refresh cycles: Operating leases are popular because they allow companies to upgrade instruments without owning aging technology.

💡 Quick Stat: The global test and measurement equipment market is projected to exceed $31 billion by 2027, driven by increasing demand for quality assurance in electronics, healthcare, and defense. Financing enables businesses to stay current with rapidly evolving technology without capital strain.

Financing vs. Leasing: Key Differences

Choosing between a loan and a lease comes down to your ownership goals, cash flow needs, and how quickly the equipment will become obsolete. Here's a detailed comparison:

| Factor | Equipment Loan (Financing) | Equipment Lease |

|---|---|---|

| Ownership | You own the equipment at end of term | Lender owns it; you have use rights |

| Monthly Payment | Higher (building equity) | Lower (paying for use) |

| End-of-Term Options | Equipment is yours | Return, renew, or buy out |

| Tax Treatment | Section 179 / bonus depreciation | Lease payments may be fully deductible |

| Obsolescence Risk | You bear the risk | Easier to upgrade at end of lease |

| Balance Sheet | Asset + liability recorded | Operating lease may stay off-balance sheet |

| Best For | Long-lived equipment with slow obsolescence | Rapidly evolving technology needing upgrades |

Rule of thumb: Finance (loan) equipment you'll use for 7+ years without significant technology change. Lease equipment that evolves rapidly — like oscilloscopes, spectrum analyzers, or diagnostic imaging systems — where next-gen models emerge every 3-5 years.

Ready to explore your options?

Crestmont Capital has helped thousands of businesses acquire the equipment they need through flexible financing and leasing programs. Get a no-obligation quote today.

Apply Now →

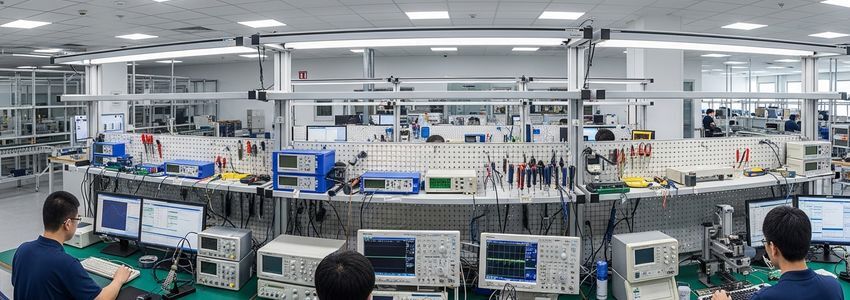

Types of Test Equipment You Can Finance or Lease

Virtually any professional testing instrument qualifies for equipment financing, provided it has identifiable value as collateral. Here are the main categories Crestmont Capital regularly finances:

Electrical & Electronic Test Equipment

- Oscilloscopes (digital, mixed-signal, high-bandwidth)

- Spectrum analyzers and signal generators

- Logic analyzers and protocol analyzers

- Multimeters, LCR meters, and impedance analyzers

- Power supplies and electronic loads

- Network analyzers (VNAs)

- EMC/EMI test systems

Mechanical & Materials Testing Equipment

- Universal testing machines (tensile, compression, bending)

- Hardness testers (Rockwell, Vickers, Brinell)

- Fatigue testing systems

- Coordinate measuring machines (CMMs)

- Torque testers and force gauges

- Vibration testing systems and shock tables

Environmental & Climatic Test Chambers

- Temperature and humidity chambers

- Thermal shock chambers

- HALT/HASS systems

- Salt spray and corrosion chambers

- UV weathering test chambers

Medical & Laboratory Test Equipment

- Diagnostic imaging systems (ultrasound, MRI components)

- Laboratory analyzers (blood, urine, chemistry)

- PCR and genomic analysis equipment

- Spectrophotometers and chromatography systems

- Microscopy systems (optical, electron, confocal)

Calibration & Metrology Equipment

- Precision calibrators

- Pressure and temperature calibration equipment

- Optical comparators and vision measurement systems

- Laser trackers and 3D scanners

Automated Test Equipment (ATE) & Systems

- In-circuit test (ICT) systems

- Functional test systems

- Semiconductor test equipment

- Flying probe testers

Not sure if your specific equipment qualifies? Contact Crestmont Capital — we work with a wide range of specialized and niche instruments.

Rates, Terms, and What to Expect in 2026

Test equipment financing rates in 2026 are competitive, particularly for businesses with established credit histories. Here's what to expect:

Loan Terms

- Loan amounts: $5,000 to $5,000,000+ (larger transactions available)

- Terms: 24 to 84 months (most common: 36-60 months)

- Interest rates: 6% to 24% APR depending on creditworthiness, time in business, and loan size

- Down payment: 0% to 20% (many lenders offer $0-down programs)

- Approval speed: Same-day to 48 hours for standard transactions; larger deals may take 3-7 business days

Lease Terms

- Lease types: Operating lease (FMV buyout), capital lease ($1 buyout), TRAC lease

- Monthly factor rates: Generally 2-5% of equipment cost per year, depending on creditworthiness

- Terms: 12 to 60 months

- End-of-lease options: Return, renew at lower rate, or purchase

What Affects Your Rate?

- Personal and business credit scores — Higher scores unlock the best rates

- Time in business — Established businesses (2+ years) get preferential rates

- Revenue and cash flow — Demonstrated ability to service debt

- Equipment type and age — New equipment from reputable manufacturers is easiest to finance

- Loan-to-value ratio — Lower LTV (larger down payment) reduces risk and rate

💡 Pro Tip: For large test systems over $250,000, Crestmont Capital can structure custom financing with extended terms, deferred payment options, or step-up payment schedules to match your cash flow. Ask about our structured finance solutions for high-value equipment.

How to Qualify for Test Equipment Financing

Qualification requirements vary by lender and loan size, but here are the general benchmarks for test equipment financing in 2026:

Standard Qualification Criteria

- Credit score: 620+ personal credit score (650+ preferred for best rates)

- Time in business: 1+ years preferred; some programs available for startups with strong credit

- Annual revenue: Generally 3-5x the annual loan/lease payments

- Down payment: 0-20% depending on credit profile and equipment type

Documents Typically Required

- Completed application (often one page for transactions under $150K)

- Equipment quote or invoice from vendor

- 3-6 months business bank statements (for larger transactions)

- Most recent 2 years business tax returns (transactions over $150K)

- Business financial statements may be required for large transactions

Startup and New Business Programs

If your business is less than 2 years old, you're not automatically disqualified. Crestmont Capital offers programs designed for newer businesses, including:

- Personal credit-based approval for transactions under $75K

- Higher down payment to offset shorter operating history

- Startup-friendly lease structures with manageable monthly payments

Get Pre-Qualified in Minutes

Crestmont Capital's online application takes less than 5 minutes. There's no hard credit pull until you accept an offer — check your options with zero risk.

Check My Rate →Tax Advantages: Section 179 and Bonus Depreciation

One of the most compelling reasons to finance test equipment rather than lease it is the ability to leverage significant tax deductions in the year of purchase.

Section 179 Deduction

Section 179 of the IRS tax code allows businesses to deduct the full purchase price of qualifying equipment in the year it's placed in service — rather than depreciating it over several years. For 2026:

- Deduction limit: Up to $1,220,000 (indexed for inflation)

- Phase-out threshold: Begins phasing out above $3,050,000 in total equipment purchases

- Applies to: New and used equipment, including financed equipment

Key point: You can finance 100% of the equipment cost but still take the full Section 179 deduction based on the equipment's value — not just the down payment.

Bonus Depreciation

In addition to Section 179, bonus depreciation allows businesses to immediately deduct a percentage of eligible new and used property. For 2026, bonus depreciation remains available (consult your tax advisor for the current applicable percentage, as it has been stepping down annually).

Lease Tax Treatment

If you choose an operating lease, lease payments are typically treated as a business expense and may be fully deductible in the year paid. This can provide consistent tax relief over the lease term without the need to capitalize the asset.

Always consult with a qualified tax professional about the best strategy for your business. The combination of financing and Section 179 can be highly effective for businesses that want both the tax deduction and ultimate ownership of the equipment.

Industries That Rely on Test Equipment Financing

Test equipment financing is used across a remarkably broad range of industries. Here are the sectors where Crestmont Capital most commonly helps businesses acquire testing instruments:

Electronics Manufacturing & PCB Assembly

Circuit board manufacturers, contract electronics assemblers, and component makers rely on in-circuit testers, flying probe systems, X-ray inspection equipment, and automated optical inspection (AOI) systems. These tools can cost $50,000 to $500,000+, making financing essential for maintaining quality control without capital strain.

Aerospace & Defense

Aerospace manufacturers and MRO (maintenance, repair, and overhaul) facilities need highly specialized environmental chambers, vibration systems, and avionics test equipment to meet FAA, MIL-SPEC, and AS9100 standards. Financing allows these businesses to maintain compliance without tying up millions in capital.

Medical Device Manufacturing & Healthcare

Medical device manufacturers must validate product safety and performance with sophisticated diagnostic equipment. Hospitals and diagnostic labs need analyzers, imaging systems, and monitoring equipment that can cost hundreds of thousands of dollars. Leasing is particularly popular in healthcare for its ability to keep equipment current.

Automotive & Transportation

Automotive manufacturers, tier suppliers, and testing labs use dynamometers, NVH (noise, vibration, harshness) systems, emissions analyzers, and crash test instrumentation. EV component testing has driven significant new investment in this sector.

Telecommunications & Networking

Telecom companies and network equipment manufacturers use signal analyzers, protocol testers, and cable certification systems to validate products and infrastructure. 5G deployments have accelerated demand for mmWave test equipment.

Research & Academic Institutions

Universities, national labs, and R&D centers often use operating leases to access cutting-edge research equipment while preserving grant budgets for research activities rather than capital purchases.

Environmental Testing & Compliance

Environmental consulting firms and industrial manufacturers use air quality monitors, water analysis equipment, soil testing instruments, and emissions monitoring systems to meet EPA and state regulatory requirements.

How to Apply for Test Equipment Financing

Applying for test equipment financing with Crestmont Capital is straightforward. Here's the step-by-step process:

- Get a vendor quote. Obtain a formal quote or invoice from your equipment vendor. You'll need the make, model, price, and vendor details.

- Submit your application. Complete Crestmont Capital's online application — it takes under 5 minutes for transactions under $150K.

- Receive your decision. Most decisions are issued within 24-48 hours. Same-day decisions are available for qualified applicants.

- Review your offer. We'll present your financing or leasing options with clear terms, monthly payment amounts, and end-of-term options.

- Sign documents. E-sign your loan or lease documents electronically.

- Equipment delivered. Once documents are signed and any down payment is received, we fund your vendor directly and your equipment is ordered/delivered.

For larger or more complex transactions (custom ATE systems, multi-unit orders, or transactions over $500K), our commercial lending team will work with you to structure the right solution.

Why Choose Crestmont Capital for Test Equipment Financing

Crestmont Capital is rated the #1 business lender in the country — and for good reason. We've built our reputation on fast approvals, transparent terms, and personalized service that big banks simply don't offer.

- Fast approvals: Decisions in as little as 24 hours for standard transactions

- Flexible structures: Loans, operating leases, capital leases, and custom structures for complex deals

- No prepayment penalties: Pay off your financing early without penalty

- Startup-friendly programs: Options for businesses under 2 years old

- Dedicated account managers: Real people who understand your business and industry

- Equipment expertise: We understand test equipment values and can often finance instruments that traditional lenders won't touch

- Soft cost bundling: Finance installation, calibration, training, and warranty alongside the hardware

Start Your Application Today

Don't let capital constraints stop you from getting the test equipment your business needs. Crestmont Capital offers fast, flexible financing for businesses of all sizes.

Apply for Equipment Financing →Frequently Asked Questions About Test Equipment Financing

What credit score do I need to finance test equipment?

Most lenders look for a personal credit score of 620 or higher. A score of 650+ will qualify you for competitive rates. Some lenders offer programs for scores as low as 580, typically with a higher down payment. Crestmont Capital works with a range of credit profiles — contact us to discuss your situation.

Can I finance used test equipment?

Yes. Most lenders, including Crestmont Capital, finance used test equipment — though terms may vary based on the equipment's age, condition, and resale value. Equipment that is current-generation, well-maintained, and traceable to a reputable manufacturer is easiest to finance. Older or highly specialized equipment may require a larger down payment.

How long does the financing process take?

For transactions under $150,000, decisions are typically made within 24-48 hours of a complete application. Same-day decisions are available for qualified applicants. Larger transactions involving custom systems or multiple units may take 3-7 business days. Once approved and documents are signed, funding typically occurs within 1-2 business days.

Can I include installation, calibration, and training in the financing?

Yes — this is called financing "soft costs." Most lenders allow you to bundle installation, calibration services, training, extended warranties, and software licenses into the equipment financing. The combined cost must represent reasonable value relative to the hardware. Crestmont Capital regularly finances these ancillary costs as part of a total project package.

What is the minimum and maximum amount I can finance?

Crestmont Capital finances test equipment from as little as $5,000 to over $5,000,000. For very large transactions or custom automated test systems, our commercial lending team can structure multi-million dollar solutions. There is no arbitrary ceiling — we evaluate each deal on its merits.

Is a down payment required?

Not always. Many borrowers with strong credit and established businesses qualify for $0 down financing on test equipment. If you have lower credit, shorter operating history, or are financing specialized equipment with limited resale value, a down payment of 10-20% may be required. A down payment also lowers your monthly payment and can improve your interest rate.

What's the difference between an FMV lease and a $1 buyout lease?

An FMV (Fair Market Value) lease has lower monthly payments because at the end of the term you have the option — not the obligation — to purchase the equipment at its fair market value at that time, return it, or renew the lease. A $1 buyout lease (also called a capital lease or finance lease) has slightly higher monthly payments, but at the end of the term you purchase the equipment for just $1. The $1 buyout is essentially a loan in lease form — you're financing the full purchase and will own it outright.

Can a startup or new business finance test equipment?

Yes, though options may be more limited. For businesses under 2 years old, Crestmont Capital offers startup equipment financing programs based on personal credit. Transactions under $75,000 may be approved based on personal credit score alone. Larger transactions for newer businesses may require a down payment or personal guarantee. Contact our team to discuss your startup's specific situation.

Can I finance test equipment from any vendor?

Generally, yes. Equipment financing is vendor-agnostic — you can purchase from any authorized dealer, OEM, manufacturer, or private seller (for used equipment). The lender will require a formal invoice or purchase agreement. Some lenders have preferred vendor programs with special rates, but Crestmont Capital works with any legitimate equipment source.

How does Section 179 apply to financed equipment?

Under Section 179, you can deduct the full purchase price of qualifying equipment in the year it's placed in service — even if you financed it. You don't need to have paid cash for the equipment. This means you can finance 100% of a $200,000 test system and potentially deduct up to the full $200,000 from your taxable income in the year of purchase (subject to income limitations and the annual deduction cap). Always verify eligibility with your tax advisor.

What happens if my business needs upgraded equipment before the lease ends?

Many equipment leases include technology refresh or upgrade provisions that allow you to swap into newer equipment partway through the lease term. Some lenders will also allow you to add the remaining balance of an existing lease into the financing for a new unit. This is one of the key advantages of leasing over purchasing outright — flexibility to stay current with rapidly evolving test technology.

What industries does Crestmont Capital serve for equipment financing?

Crestmont Capital serves businesses across all industries that require test and measurement equipment — including electronics manufacturing, aerospace and defense, healthcare and medical devices, automotive, telecommunications, construction, environmental testing, research and academia, and many more. We are industry-agnostic and evaluate each application based on the business's financial profile, not its sector.

Are there prepayment penalties on equipment loans?

Crestmont Capital does not charge prepayment penalties on equipment loans. You can pay off your loan early and stop accruing interest without any additional fees. Note that operating leases are typically structured as a commitment for the full term — early termination provisions vary and should be reviewed carefully before signing.

Can I apply online?

Yes. Crestmont Capital's online application is available 24/7 at crestmontcapital.com/apply. The application takes less than 5 minutes for standard transactions under $150,000. A dedicated account manager will review your application and contact you to discuss your options — typically within one business day.

What makes Crestmont Capital different from a bank for equipment financing?

Traditional banks are slow, document-heavy, and often decline equipment financing for newer businesses, specialized equipment, or businesses with imperfect credit. Crestmont Capital is an alternative lender focused specifically on business equipment — meaning faster approvals, more flexible credit criteria, and account managers who understand equipment values and industry dynamics. We've earned our #1 national rating by consistently getting deals done that banks turn away.

Disclaimer: The information provided in this article is for general educational purposes only and is not financial, legal, or tax advice. Funding terms, qualifications, and product availability may vary and are subject to change without notice. Crestmont Capital does not guarantee approval, rates, or specific outcomes. For personalized information about your business funding options, contact our team directly.