HVAC contractor business loans give heating, ventilation, and air conditioning companies the capital to expand their service van fleet, purchase diagnostic equipment, manage extreme seasonal cash flow swings, and scale into commercial contracts — without waiting months for a bank decision. Whether you run a two-van residential HVAC operation or a 25-technician commercial HVAC company, HVAC company financing from Crestmont Capital provides $10,000 to $1,000,000 in fast, flexible capital tailored to the unique demands of the HVAC industry.

The HVAC business is defined by two brutal realities: extreme demand peaks in summer and winter, and the enormous capital investment required to capitalize on those peaks. Service vans cost $35,000–$65,000 each. Refrigerant stock runs $5,000–$20,000 per technician annually. Commercial diagnostic equipment — manifold gauges, leak detectors, refrigerant recovery machines, ductwork analyzers — can cost $15,000–$40,000 per service truck. And when the peak season hits, you need every van fully stocked and operational, every technician equipped, and every commercial contract staffed — or your competitors take the jobs. According to the Air Conditioning Contractors of America (ACCA), the HVAC industry employs over 400,000 technicians and generates more than $115 billion in annual revenue in the United States — making it one of the fastest-growing skilled trades in the country.

Running a successful HVAC company is one of the most capital-intensive small business propositions in the skilled trades. The combination of expensive equipment, volatile refrigerant costs, seasonal demand extremes, and rapid technology change creates a near-constant need for working capital and strategic financing. Understanding these structural challenges — and how to address them with the right financing products — is the difference between an HVAC company that grows and one that struggles.

Several structural features of the HVAC business drive financing needs that most other service industries don't face to the same degree:

According to the U.S. Small Business Administration (SBA), HVAC contractors are consistently among the top skilled trades applying for small business financing — a direct reflection of the industry's structural capital intensity. Forbes and CNBC have both highlighted HVAC as one of the most resilient and high-demand skilled trades in the U.S. economy, with labor shortages driving strong pricing power and revenue growth for established HVAC businesses.

Fast approvals. All HVAC company types. $10K to $1M available.

Apply Now →No industry experiences demand volatility more extreme than HVAC. When temperatures spike above 95°F in July, every residential air conditioner in your service area is running at full capacity — and a meaningful percentage will fail simultaneously. When temperatures drop below 20°F in January, heating systems that haven't been serviced in two years push their components to the breaking point. These twin demand peaks — summer cooling emergencies and winter heating emergencies — represent both the greatest revenue opportunity and the greatest operational challenge HVAC contractors face.

In most U.S. markets, HVAC companies generate 40–60% of their annual revenue from May through August. A single heat wave — three or more days above 95°F — can generate more service calls than a normal two-week period. HVAC companies that are fully staffed, fully stocked with parts (capacitors, contactors, blower motors, refrigerant), and operating maximum vans capitalize enormously on these events. Companies that run out of common parts mid-heat-wave lose hundreds of thousands of dollars in emergency service revenue to competitors.

Preparing for summer peak season requires capital deployed weeks in advance — parts inventory ($15,000–$40,000 for a 5-van operation), refrigerant stock ($8,000–$20,000), additional technician hiring and onboarding, and marketing to lock in maintenance contract renewals. A short-term business loan or business line of credit deployed in April or May — before peak season revenue arrives — is often the highest-ROI financing decision an HVAC company can make.

The second HVAC peak season — winter heating — follows a similar pattern. When the first polar vortex of the season arrives, furnaces, boilers, and heat pumps that have been dormant since March suddenly face maximum load. Failure rates spike, and every HVAC company in the market is fielding emergency service calls simultaneously. The companies that win the most emergency heating business have technicians on call, parts stocked (heat exchangers, ignitors, flame sensors, pressure switches, blower motors), and vans available — not waiting on distributor back-orders.

Between summer and winter peaks — particularly during the spring shoulder season (March–May) and fall shoulder season (September–October) — HVAC service call volume drops significantly. Residential maintenance calls continue, but emergency service revenue dries up. During these shoulder seasons, HVAC companies must manage fixed costs (van payments, insurance, office overhead, technician base wages) on reduced revenue. Without adequate working capital reserves or access to credit, HVAC contractors are forced to reduce staff, defer equipment maintenance, and miss the preparation window for the next peak season.

Smart HVAC companies use financing to level the seasonal cash flow curve: drawing on a line of credit during shoulder seasons to maintain operations and prepare for peaks, then repaying during peak-season revenue. This disciplined approach transforms seasonal volatility from a threat into a manageable business rhythm.

The capital investment required to field a single HVAC technician is substantial. Unlike many service businesses where a skilled worker and a vehicle are sufficient, HVAC technicians require specialized equipment, diagnostic tools, refrigerant stock, and a comprehensive parts inventory that together represent a $55,000–$95,000 investment per van. HVAC equipment financing allows companies to spread this cost over 48–84 months while immediately deploying the asset to generate revenue.

| Item | Typical Cost | Financing Term | Notes |

|---|---|---|---|

| Service Van (Ram ProMaster, Ford Transit, etc.) | $35,000–$65,000 | 48–84 months | Primary HVAC work vehicle |

| Van Shelving & Organization Systems | $3,000–$8,000 | 24–60 months | Adrian Steel, Weather Guard, etc. |

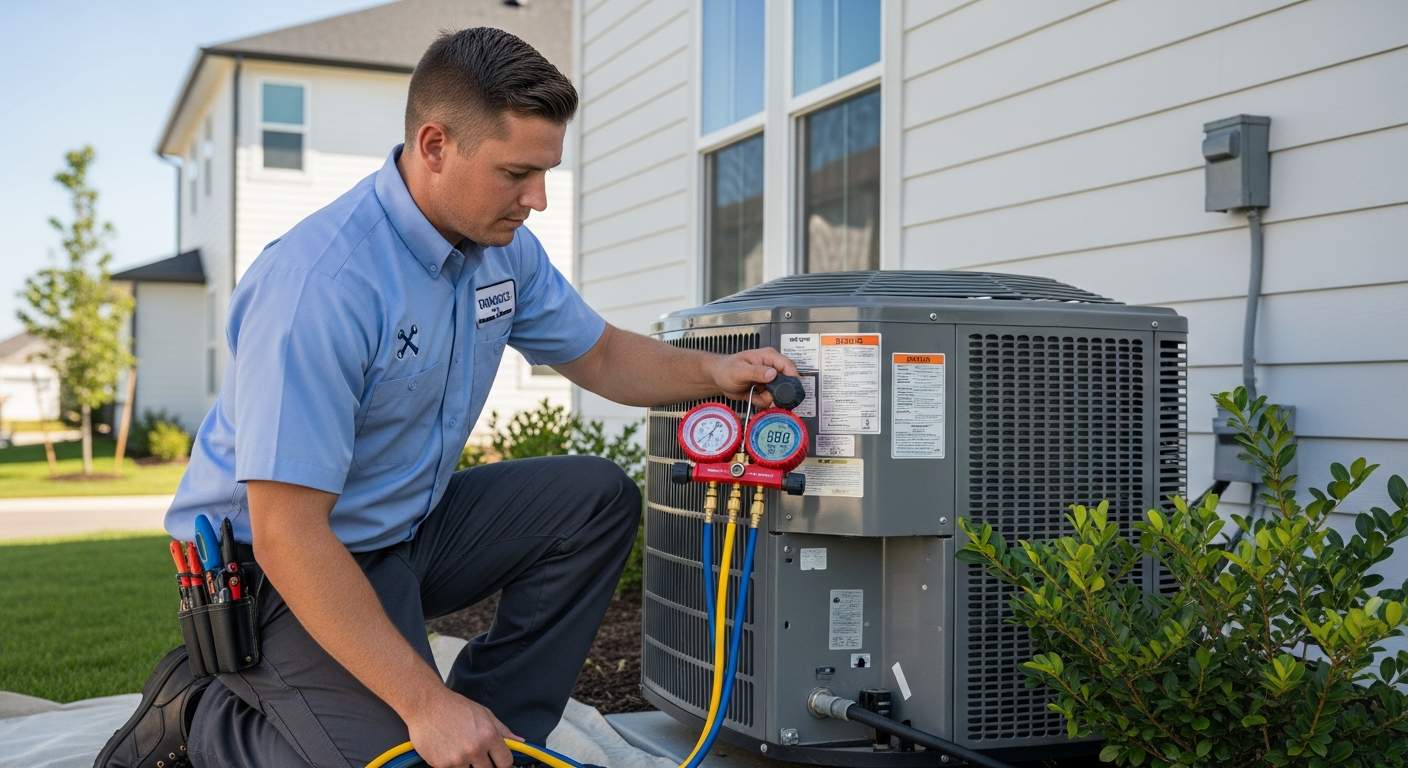

| Refrigerant Recovery Machine | $1,500–$4,500 | 24–48 months | EPA Section 608 required |

| Digital Manifold Gauge Set | $500–$2,500 | 24–36 months | Testo, Fieldpiece, JB Industries |

| Combustion Analyzer | $800–$3,500 | 24–36 months | Required for gas furnace service |

| Refrigerant Leak Detector | $300–$1,500 | 12–24 months | Electronic; needed per tech |

| Vacuum Pump (2-stage) | $300–$1,200 | 12–24 months | System commissioning & service |

| Initial Parts Inventory (per van) | $8,000–$20,000 | 12–36 months | Capacitors, contactors, motors, boards |

| Refrigerant Stock (R-410A, R-32, R-22) | $3,000–$12,000 | 12–24 months | Volatile pricing; buy strategically |

| Ductwork Analysis Equipment | $2,000–$8,000 | 24–48 months | Energy auditing; premium services |

| Full Van Buildout (all-in) | $55,000–$95,000 | 48–84 months | Complete technician deployment package |

When you multiply the cost of a full van buildout ($55,000–$95,000) by the number of technicians you need to staff a peak season, the capital requirement becomes substantial. A company adding 3 fully equipped technicians for summer peak season needs $165,000–$285,000 in equipment investment alone — before a single air conditioner is repaired. Equipment financing allows you to deploy those assets in April and begin generating revenue immediately while spreading payments over 5–7 years.

Crestmont Capital offers multiple financing solutions tailored to the HVAC industry's specific needs. Here are the primary loan types available to HVAC contractors:

HVAC equipment financing covers service vans, van shelving, refrigerant recovery machines, digital manifold sets, combustion analyzers, vacuum pumps, diagnostic equipment, and any other equipment your technicians need. The equipment being purchased serves as collateral, resulting in lower rates and higher approval rates compared to unsecured products. Terms from 24 to 84 months. You own the equipment from day one — no end-of-term purchase options required. Finance one van or an entire fleet simultaneously.

Working capital loans for HVAC companies provide fast, flexible cash for operational needs — parts inventory purchasing, refrigerant stock, technician payroll during shoulder seasons, spring and fall ramp-up capital, and marketing. Unsecured working capital loans fund within 24–48 hours with no equipment or real estate collateral required. Amounts from $10,000 to $500,000 depending on revenue and creditworthiness. Most commonly used by residential HVAC contractors managing seasonal cash flow.

Heat waves don't give advance notice. When temperatures spike and your service schedule books out 3 weeks ahead overnight, you need capital immediately to stock parts, bring on additional technicians, and keep every van operational. Fast business loans from Crestmont Capital are approved and funded within 24 hours. Minimal documentation — 3 months of bank statements and a one-page application. Amounts from $10,000 to $500,000. Designed for HVAC companies that need to move at the speed of peak season demand.

Short-term business loans provide a fixed lump sum with repayment over 3 to 18 months — ideal for seasonal bridge financing, pre-season ramp-up capital, or a specific large commercial contract mobilization. Unlike lines of credit, short-term loans provide the full amount upfront, making them well-suited for HVAC contractors with a specific capital need and a predictable repayment timeline tied to seasonal revenue. Amounts from $10,000 to $500,000.

A business line of credit is the most flexible financing tool for seasonal HVAC businesses. Draw what you need, when you need it. Pay interest only on what you've drawn. As you repay, the credit becomes available again — perfectly matching the recurring seasonal pattern of the HVAC industry. Draw in March to stock parts for summer, repay in August when peak season revenue floods in, draw again in September to prepare for winter heating season. Lines from $25,000 to $500,000 for qualifying HVAC companies.

HVAC contractors with 2+ years in business, strong revenue, and 680+ personal credit scores may qualify for SBA 7(a) loans up to $5 million. SBA loans offer the most favorable terms available to small businesses — rates and repayment periods that traditional commercial loans can't match. The tradeoff is time: SBA approvals take 30–90 days, making them best suited for planned fleet expansions or major facility investments rather than urgent capital needs. Visit SBA.gov for eligibility requirements.

Past credit challenges don't disqualify HVAC contractors from business financing. Bad credit business loans from Crestmont Capital are available to HVAC companies with personal credit scores as low as 500, provided the business demonstrates sufficient revenue and cash flow. Revenue-based approval evaluates your bank deposits, job volume, and business history — not just your FICO score. Many successful HVAC contractors with thriving businesses have past personal credit events that don't reflect current business performance.

| Loan Type | Amount Range | Best For | Rate Range | Term | Speed |

|---|---|---|---|---|---|

| Equipment Financing | $5K–$500K | Vans, tools, diagnostic equipment | 6–14% APR | 24–84 months | 3–7 days |

| Working Capital Loan | $10K–$500K | Parts, refrigerant, seasonal ops | 8–25% APR | 6–18 months | 24–48 hrs |

| Fast Business Loan | $10K–$500K | Urgent peak season capital | 8–25% APR | 6–18 months | 24 hrs |

| Short-Term Loan | $10K–$500K | Seasonal bridge, commercial ramp-up | 8–22% APR | 3–18 months | 1–3 days |

| Business Line of Credit | $25K–$500K | Revolving seasonal capital | 7–20% APR | Revolving | 3–7 days |

| SBA Loan | $50K–$5M | Major fleet/facility expansion | Prime + 2.75–4.75% | Up to 10 years | 30–90 days |

| Bad Credit Business Loan | $10K–$250K | HVAC contractors with credit issues | 12–35% APR | 6–24 months | 24–48 hrs |

Rates vary based on creditworthiness, loan amount, term, and business revenue. Contact Crestmont Capital for a personalized quote.

Crestmont Capital evaluates HVAC company loan applications on a combination of business revenue, credit history, and time in business. Here's what lenders typically look for:

| Requirement | Working Capital / Fast Loans | Equipment Financing | Small Business Loans |

|---|---|---|---|

| Time in Business | 3+ months | 6+ months | 1+ year |

| Annual Revenue | $75K+ | $100K+ | $150K+ |

| Personal Credit Score | 500+ (flexible) | 550+ | 580+ |

| Monthly Bank Deposits | $6,000+ | $8,000+ | $12,500+ |

| Collateral Required | No (unsecured) | Equipment only | Varies |

| Documents Required | 3 months bank statements | 3–6 months + equipment quote | 6+ months + tax returns |

A frequently asked question from HVAC contractors: "Will lenders penalize me for low revenue during shoulder seasons?" At Crestmont Capital, the answer is no. Our underwriting team specializes in seasonal business cycles. We look at 12-month trailing revenue, annual patterns, and peak-season performance to determine financing capacity. An HVAC company generating $600,000 from May through August and December through February — with lighter shoulder seasons — is evaluated on its full annual revenue picture, not its slowest month.

| Loan Program | Interest Rate Range | Typical Term | Funding Speed | Typical Use |

|---|---|---|---|---|

| Working Capital (Unsecured) | 8–25% APR | 6–18 months | 24–48 hours | Parts, refrigerant, payroll |

| Fast Business Loan | 8–25% APR | 6–18 months | 24 hours | Urgent peak season capital |

| Equipment Financing (Vans) | 6–14% APR | 48–84 months | 3–7 days | Service vans, fleet vehicles |

| Equipment Financing (Tools/Diagnostics) | 7–16% APR | 24–60 months | 3–5 days | Manifold sets, analyzers, recovery machines |

| Short-Term Business Loan | 8–22% APR | 3–18 months | 1–3 days | Seasonal bridge, commercial ramp-up |

| Small Business Loan | 7–22% APR | 12–60 months | 2–5 days | Expansion, commercial entry |

| Business Line of Credit | 7–20% APR | Revolving | 3–7 days | Recurring seasonal capital |

| Bad Credit Business Loan | 12–35% APR | 6–24 months | 24–48 hours | Credit-challenged HVAC contractors |

Rates are illustrative. Actual rates depend on creditworthiness, revenue, loan amount, term, and collateral. Crestmont Capital will provide your exact rate in a formal term sheet before any commitment is required.

Complete Crestmont Capital's fast online application at offers.crestmontcapital.com. Provide basic business information, approximate annual revenue, and how much you need. No long forms, no commitment required. Takes about 5 minutes.

For working capital and fast loans: 3 months of business bank statements and a government-issued ID. For equipment financing: add an equipment quote or van listing. For larger loans: 6 months of bank statements and your most recent business tax return. Your advisor will guide you through exactly what's needed for your specific loan type.

Crestmont Capital's underwriting team reviews your application and documents, then provides a decision — for working capital loans, typically within 24 hours of receiving complete documents. Equipment financing takes 3–5 business days. You'll receive a clear term sheet showing your approved amount, rate, term, and monthly payment. No surprises.

Review your loan offer carefully. Compare it to any other options you're considering. Ask your advisor questions. There's no pressure and no obligation until you sign. Crestmont Capital offers transparent terms — what you see in the term sheet is what you get.

Working capital and fast loans fund directly to your business bank account within 24–48 hours of signing. Equipment financing funds to the dealer or vendor. Your new financing is in place — stock parts, acquire vans, hire technicians, and be fully ready when peak season arrives.

Different HVAC business models have different financing needs. Crestmont Capital works with all HVAC company types:

| Company Type | Common Financing Uses | Typical Loan Range | Key Considerations |

|---|---|---|---|

| Residential HVAC | Service vans, parts inventory, seasonal WC | $10K–$300K | High service call volume; extreme seasonal peaks |

| Commercial HVAC | Large equipment, fleet expansion, contract ramp-up | $50K–$1M | Longer payment cycles; rooftop unit & chiller systems |

| Refrigeration Contractors | Specialized tools, refrigerant stock, diagnostics | $25K–$500K | Commercial refrigeration; grocery & food service focused |

| Sheet Metal / Ductwork | Plasma cutters, fabrication equipment, vehicles | $25K–$750K | Equipment-intensive; often commercial subcontracting |

| Plumbing + HVAC Combo | Combined fleet, dual-service parts inventory | $25K–$750K | Multiple revenue streams; stronger off-season revenue |

| HVAC Installation Specialist | Equipment, temporary labor, materials pre-buy | $25K–$500K | Project-based revenue; milestone payment structure |

| Owner-Operator / Solo Tech | First van, tool financing, working capital | $10K–$150K | Personal credit important; revenue history may be short |

Sources: ACCA, IBISWorld, U.S. BLS, SBA, Crestmont Capital Research

These scenarios reflect the types of HVAC contractor loans Crestmont Capital funds. Business names and identifying details have been changed for privacy.

A residential HVAC company in the Southwest had grown from 2 to 5 technicians over three years and was turning down service calls every summer due to van capacity. The owner identified the need to add 3 fully equipped service vans — Ford Transit 250 cargo vans at $42,000 each, van shelving at $4,500 per unit, and initial parts/tool packages at $9,500 per van — totaling $168,000 for the full fleet addition. He financed $165,000 through Crestmont Capital's equipment financing program over 72 months. The three additional vans allowed him to add 3 full-time technicians. In the first full peak season, the three new techs generated $390,000 in combined revenue. The fleet expansion paid for itself in the first year and has continued generating strong returns each subsequent season.

An HVAC contractor in the Southeast had been losing commercial maintenance bids to a competitor who offered advanced energy auditing and system performance diagnostics. To compete, she needed to invest in commercial-grade diagnostic equipment: a portable data logger system ($12,000), duct blaster testing kit ($8,500), combustion analyzer upgrade ($3,200), digital manifold upgrades for all 4 service vans ($6,800), and a refrigerant charging scale and recovery station upgrade ($7,500) — totaling $38,000, with additional training costs bringing the total need to $45,000. She financed $45,000 through a working capital loan, funded within 36 hours. With the new diagnostic capabilities, she won 4 commercial maintenance contracts in the following 60 days, generating $72,000 in annual recurring revenue. The loan paid for itself in the first 8 months.

A mid-size HVAC company in the Midwest operated with 8 technicians through peak season but consistently hit a cash flow crunch each March when winter maintenance revenue slowed but summer prep costs were accelerating. The owner needed to hire 3 seasonal technicians (payroll deposit + onboarding: $18,000), purchase summer parts inventory (capacitors, contactors, blower motors, refrigerant: $28,000), renew all service agreement marketing campaigns ($12,000), and service the entire van fleet before the summer rush ($9,000) — totaling $67,000. He secured a $75,000 short-term bridge loan in March, giving him a buffer for unexpected costs. Peak season revenue repaid the loan in full by July. The disciplined use of a seasonal bridge loan is now a standard part of his annual financial planning cycle.

A residential HVAC contractor in Texas had received interest from two commercial property management companies seeking full-service HVAC maintenance contracts covering 14 commercial buildings with rooftop units. To service commercial RTUs at scale, she needed a bucket truck/aerial lift ($65,000), two additional full-size service vans ($82,000), a commercial rooftop unit diagnostic and testing package ($24,000), increased refrigerant inventory ($18,000), and 90 days of additional technician payroll while contracts ramped up ($31,000) — totaling $220,000. She secured a $220,000 equipment and working capital package from Crestmont Capital, structured as $150,000 in equipment financing (72 months) and $70,000 in working capital (18 months). The two commercial property management contracts generated $285,000 in year one, with recurring annual revenue well in excess of the financing cost.

| Lender Type | Amount Range | Approval Speed | Seasonal Revenue Flexibility | Credit Flexibility |

|---|---|---|---|---|

| Crestmont Capital | $10K–$1M | 24 hrs–7 days | High — evaluates annual patterns | High (500+ FICO) |

| Traditional Banks | $50K+ | 30–90 days | Low — requires consistent monthly revenue | Low (680+ FICO) |

| Credit Unions | $10K–$200K | 2–4 weeks | Moderate | Moderate (640+) |

| Online Lenders (non-specialist) | $5K–$500K | 1–3 days | Low — algorithmic scoring | Moderate (580+) |

| Equipment Dealers (in-house) | $5K–$200K | 1–3 days | Low | Moderate |

| SBA (via bank) | $50K–$5M | 30–90 days | Moderate with documentation | Moderate (640+) |

Crestmont Capital is rated the #1 small business lender in the United States. HVAC contractors across the country choose us for HVAC company financing because we understand your business — the seasonal peaks, the equipment investment, the refrigerant costs, the commercial contract opportunities — not just your credit score.

Equipment financing, working capital, fleet loans, and seasonal bridge financing for HVAC companies of all sizes.

Apply in 5 Minutes →HVAC contractor business loans are commercial financing products designed for heating, ventilation, and air conditioning companies of all sizes — from solo owner-operators to large commercial HVAC firms. These loans provide capital for service van and equipment purchases, parts and refrigerant inventory, technician payroll, seasonal working capital, and commercial contract mobilization. Types include equipment financing, working capital loans, short-term loans, lines of credit, and SBA loans. Crestmont Capital offers HVAC business loans from $10,000 to $1,000,000.

HVAC companies can borrow from $10,000 for basic working capital needs up to $1,000,000 for major fleet expansion or commercial market entry. The amount you qualify for depends on your annual revenue, time in business, credit history, and loan type. An HVAC company with $400,000 in annual revenue and 2+ years in business typically qualifies for $60,000–$200,000 in working capital or equipment financing. Contact Crestmont Capital for a personalized assessment based on your specific situation.

Crestmont Capital considers HVAC business loan applications with personal credit scores as low as 500 for revenue-based working capital products. Equipment financing generally requires 550+. Small business term loans are available at 580+ with strong revenue. Bad credit business loans are specifically designed for HVAC contractors with past credit challenges — collections, prior defaults, or thin credit history — who have strong current business revenue. A higher credit score will earn better rates and terms, but poor credit alone does not disqualify you.

Yes. Service van and fleet financing is one of the most common uses for HVAC business loans from Crestmont Capital. Equipment financing for HVAC vans uses the vehicle as collateral — resulting in lower rates (typically 6–14% APR) and longer terms (48–84 months) compared to unsecured working capital products. You can finance a single van or an entire fleet simultaneously. A fully equipped HVAC service van costs $55,000–$95,000; financing over 72 months keeps cash in your business for parts, refrigerant, and operations while the van generates revenue immediately.

Crestmont Capital's fast business loans and working capital loans are approved in 24 hours and funded within 24–48 hours of signing. Equipment financing takes 3–7 business days. Small business term loans typically close in 2–5 business days. For HVAC contractors who need capital to respond to a heat wave, a cold snap, or a sudden commercial contract opportunity, Crestmont Capital's 24-hour approval process matches the speed your business requires.

HVAC business loans can be used for virtually any legitimate business purpose, including: purchasing service vans, trailers, and work vehicles; buying diagnostic equipment (manifold gauges, combustion analyzers, leak detectors, recovery machines); stocking parts inventory (capacitors, contactors, motors, circuit boards); purchasing refrigerant (R-410A, R-32, R-22 reclaim); covering technician payroll and benefits during shoulder seasons; funding commercial HVAC contract mobilization; marketing and customer acquisition; hiring and training additional technicians; and bridging the seasonal cash flow gap between peak seasons.

Yes. HVAC contractors qualify for SBA 7(a) small business loans, which offer amounts up to $5 million with repayment terms up to 10 years for working capital and equipment. SBA loans offer some of the most favorable rates available to small businesses. Requirements include 2+ years in business, 680+ personal credit score, and detailed financial documentation including tax returns. The application and approval process takes 30–90 days — making SBA loans best suited for planned fleet expansions or commercial market entry rather than urgent peak season capital needs. Visit SBA.gov for full eligibility requirements.

New HVAC companies can qualify for financing with as little as 3 months in business for revenue-based working capital products. The key requirement for newer businesses is demonstrating sufficient revenue — typically $6,000+ per month in bank deposits. Equipment financing for newer companies is also available when there's a specific asset to secure the loan. HVAC startups with less than 3 months of history face more limited options; in those cases, equipment financing with personal guarantees and strong personal credit is often the best path to early-stage capital.

HVAC's dual seasonal revenue pattern is well understood by Crestmont Capital's underwriting team. We evaluate your annual revenue total and seasonal patterns — not just the most recent 30 or 90 days. An HVAC company with strong summer and winter revenue but lighter shoulder season deposits is evaluated on its full annual performance. Providing 12 months of bank statements is the most effective way to ensure your seasonal business is fully credited. A business line of credit is specifically designed for seasonal businesses — draw during slow months, repay during peak season revenue.

Working capital loans and business lines of credit are the most commonly used financing products for refrigerant and parts inventory purchases. These are short-term, liquid financing tools that match the inventory cycle — you deploy the capital to stock up before peak season, then repay from peak-season revenue. For large one-time refrigerant purchases (taking advantage of price drops), a short-term working capital loan is often most efficient. For ongoing, recurring inventory needs, a revolving business line of credit provides maximum flexibility — draw when you need to stock up, repay as jobs generate revenue.

Document requirements vary by loan type. For working capital and fast loans: 3 months of business bank statements, government-issued ID, and basic business information (EIN, address, monthly revenue estimate). For equipment financing: add an equipment quote, van listing, or dealer invoice. For small business term loans: 6 months of bank statements, most recent business and personal tax returns, and details on intended use. For commercial contract financing: provide the contract documentation. Crestmont Capital's advisors will guide you through the specific requirements — we aim to keep the process as simple as possible.

Yes. Commercial HVAC equipment financing for rooftop units (RTUs), chillers, air handlers, VRF systems, and other large commercial equipment is available through Crestmont Capital. Commercial equipment financing typically requires 6+ months in business and $150,000+ in annual revenue. The commercial equipment being financed serves as collateral. For large commercial projects, equipment and working capital packages can be structured to cover both the equipment investment and the operational capital needed to service the contracts the equipment supports.

Expanding from residential to commercial HVAC is one of the highest-ROI moves an HVAC company can make — but it requires meaningful upfront capital: specialized commercial equipment, additional technicians, refrigerant stock for larger systems, and often an aerial lift or bucket truck for rooftop unit access. A combined equipment and working capital package from Crestmont Capital can fund the full commercial expansion in one financing event — equipment loans for the physical assets (72–84 month terms) and a working capital component for the operational ramp-up period (12–18 month terms). Contact a Crestmont advisor to structure the right commercial expansion package for your specific situation.